Econometrics I

TA Christian Alemán

Session 4: Friday 11, February 2022

Based on Prof.Michael Creel's Lecture Notes And Fumio Ayashi's Book Econometrics section 1.7

Activity 1: "Replicating Nerlove"

Nerlove’s 1963 paper is a classic study of returns to scale in a regulated industry.

Firms Minimize Cost:

Subject to a Constant Returns to Scale Production Function (Cobb-Douglas)

Where  are the inputs, labor, fuel and capital respectively.

are the inputs, labor, fuel and capital respectively.

Equilibirum prices are respectively  .

.

Recall that we have constant returns to scale if:

Solving the minization problem we find that the Cost Function is also Cobb-Douglas:

Whats more, the cost function above will be homogeneous of degree 1 (HOD1) if

We can rewrite the above cost function as:

Take the logs

Our Data

Data on Company's:

- COST(C)

- OUTPUT(Q)

- PRICE OFLABOR

- PRICE OF FUEL

- PRICE OF CAPITAL

.

.

We are ready to run some tests!

We want to test:

- Constant Returns to Scale (CRS) assumption

- Homogeneity of degree 1

- Understant whether CRS changes with size of the company

Our Tools:

- Restricted estimation:

- Testing: Chow-test

% Housekeeping clc close all clear all % Load the Data load nerlove data = data(:,2:6); data = log(data); n = size(data,1); y = data(:,1); x = data(:,2:5); x = [ones(n,1), x]; k = size(x,2); names = str2mat("constant", "output","labor", "fuel", "capital"); names = [names; names; names; names; names]; % copy 5 times for Chow test % Run OLS [b,~,~,~] = mc_ols(y,x,names, 0, 1);

********************************************************* OLS estimation results Observations 145 R-squared 0.925955 Sigma-squared 0.153943 Results (Ordinary var-cov estimator) estimate st.err. t-stat. p-value 1 -3.527 1.774 -1.987 0.049 2 0.720 0.017 41.244 0.000 3 0.436 0.291 1.499 0.136 4 0.427 0.100 4.249 0.000 5 -0.220 0.339 -0.648 0.518 *********************************************************

Activity 2: Testing

Testing Homogeneity of Degree 1

Recall the linear restriction form:

In our case for HOD1 we need  and

and

The null hypothesis for qF,Wald,LR test below is:

We cannot reject the null (the p-value is above 0.05), meaning that we cannot reject Homogeneity

% First Homogeneity of Degree 1 (HOD1) R = [0, 0, 1, 1, 1]; r = 1; % Imposing and testing HOD1 mc_olsr(y, x, R, r, names); TestStatistics(y, x, R, r);

For some reason the output of this example is comming at the end of the page.

Testing Constant Returns to scale (CRS)

In our case for CRS we need and

We reject the null (the p-value is below 0.05), meaning that we reject the assumption of constant returns to scale.

% Now Constant Returs to Scale (CRTS) R = [0, 1, 0, 0, 0]; r = 1; % Imposing and testing CRTS mc_olsr(y, x, R, r, names); TestStatistics(y, x, R, r);

Restricted LS estimation results

Observations 145

R-squared 0.790420

Sigma-squared 0.438861

Results (Het. consistent var-cov estimator)

estimate st.err. t-stat. p-value

1 -7.530 2.919 -2.579 0.011

2 1.000 0.000 Inf 0.000

3 0.020 0.376 0.052 0.959

4 0.715 0.159 4.490 0.000

5 0.076 0.576 0.132 0.896

*********************************************************

Value p-value

F 256.262 0.000

Wald 265.414 0.000

LR 150.863 0.000

Score 93.771 0.000

Activity 3: The chow test

We want to understant whether CRS changes with size of the company

Define 5 subsamples of firms, with thefirst group being the 29 firms with the lowest output levels, then the next 29 firms, etc.

To do this define dummy variables:

Otherwise

Otherwise

Otherwise

Otherwise

And so forth fro

Then the model can be rewritten as:

In Matrix form

![$\left[\begin{array}{c}y_{1} \\ y_{2} \\ y_{3} \\ y_{4} \\ y_{5} \end{array}\right]=\left[\begin{array}{ccccc}X_{1}&0&0&0&0 \\ 0&X_{2}&0&0&0 \\ 0&0&X_{3}&0&0 \\ 0&0&0&X_{4}&0 \\ 0&0&0&0&X_{5} \end{array}\right]\left[\begin{array}{c}\beta^{1} \\ \beta^{2} \\ \beta^{3} \\ \beta^{4} \\ \beta^{5} \end{array}\right]\left[\begin{array}{c}\epsilon_{1} \\ \epsilon_{2} \\ \epsilon_{3} \\ \epsilon_{4} \\ \epsilon_{5} \end{array}\right]$](s4_eq03914849164482470231.png)

We define

% Create the block diagonal X matrix corresponding to separate coefficients big_x = zeros(n,5*k); %x_A = NaN() x_old = x; for i=1:k startrow = (i-1)*29+1; endrow = i*29; startcol =(i-1)*k + 1; endcol = i*k; big_x(startrow:endrow,startcol:endcol) ... = big_x(startrow:endrow,startcol:endcol)... + x(startrow:endrow,:); % Alternative X % x_A(:,:,i) = x(startrow:endrow,:); end x = big_x;

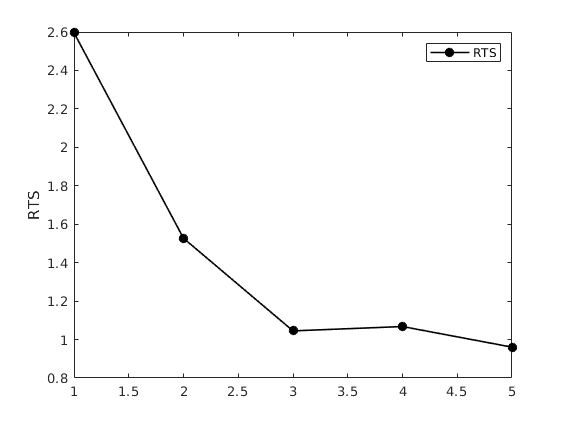

Visual Inspection

Nerlove model: 5 separate regressions, one per each group of firms

b = mc_ols(y, x, names); output = 1:5; output = output*5+2-5; % Just extract the relevant parameter output = b(output,:); rts = 1 ./ output; % gset term X11 xlabel("Output group"); group = 1:5; figure(1) plot(group, rts,"ko-",'linewidth',1.2,'markerfacecolor','k') ylabel('RTS') legend('RTS')

*********************************************************

OLS estimation results

Observations 145

R-squared 0.960901

Sigma-squared 0.094836

Results (Het. consistent var-cov estimator)

estimate st.err. t-stat. p-value

constant 0.390 4.049 0.096 0.923

output 0.385 0.089 4.315 0.000

labor -0.177 0.894 -0.198 0.844

fuel 0.406 0.255 1.591 0.114

capital -0.650 0.744 -0.873 0.384

constant -0.569 1.937 -0.294 0.769

output 0.655 0.077 8.490 0.000

labor -0.522 0.284 -1.834 0.069

fuel 0.511 0.090 5.669 0.000

capital -0.681 0.375 -1.819 0.071

constant -2.146 1.724 -1.245 0.216

output 0.957 0.135 7.095 0.000

labor -0.335 0.208 -1.610 0.110

fuel 0.409 0.120 3.408 0.001

capital -0.722 0.264 -2.739 0.007

constant -4.934 1.732 -2.849 0.005

output 0.937 0.106 8.865 0.000

labor 0.313 0.238 1.313 0.192

fuel 0.439 0.061 7.206 0.000

capital -0.255 0.293 -0.871 0.386

constant -6.946 1.828 -3.800 0.000

output 1.041 0.064 16.339 0.000

labor 0.642 0.228 2.818 0.006

fuel 0.679 0.097 7.039 0.000

capital -0.239 0.288 -0.830 0.408

*********************************************************

Chow test

When performing the Chow Tets the null to test is that the parameter vectors for the separate groups are all the same, that is:

We reject the null, then the estimated coefficients are different for the 5 groups.

R = eye(5);

Z = zeros(5,5);

R = [

R -R Z Z Z;

R Z -R Z Z;

R Z Z -R Z;

R Z Z Z -R

];

r = zeros(20,1);

% Chow test:

mc_olsr(y, x, R, r, names);

TestStatistics(y, x, R, r);

Restricted LS estimation results

Observations 145

R-squared 0.925955

Sigma-squared 0.215520

Results (Het. consistent var-cov estimator)

estimate st.err. t-stat. p-value

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

*********************************************************

Value p-value

F 5.363 0.000

Wald 129.601 0.000

LR 92.595 0.000

Score 68.434 0.000

Pick another reference, results should be the same

Chow test: note that the restricted model gives the same results as the original model

R = eye(5); Z = zeros(5,5); R = [ -R Z Z Z R; Z -R Z R Z; Z Z -R Z R; -R R Z Z Z ]; r = zeros(20,1); mc_olsr(y, x, R, r, names); TestStatistics(y, x, R, r);

Restricted LS estimation results

Observations 145

R-squared 0.925955

Sigma-squared 0.215520

Results (Het. consistent var-cov estimator)

estimate st.err. t-stat. p-value

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

constant -3.527 1.689 -2.088 0.039

output 0.720 0.032 22.491 0.000

labor 0.436 0.241 1.808 0.074

fuel 0.427 0.074 5.751 0.000

capital -0.220 0.318 -0.691 0.491

*********************************************************

Value p-value

F 5.363 0.000

Wald 129.601 0.000

LR 92.595 0.000

Score 68.434 0.000

Run the Chow test only the last two groups:

% Trim the data % ng: Choose number of groups : % ng = 2; ni = 5-ng; y = y(29*ni+1:end,1); x = x(29*ni+1:end,5*ni+1:end); R = eye(5); Z = zeros(5,5); R = [R -R]; r = zeros(5*(ng-1),1);

Chow test: note that we still reject the null, but only at the 95% level, not at 90% anymore

mc_olsr(y, x, R, r, names); TestStatistics(y, x, R, r);

Restricted LS estimation results

Observations 58

R-squared 0.961866

Sigma-squared 0.026330

Results (Het. consistent var-cov estimator)

estimate st.err. t-stat. p-value

1 -5.526 1.437 -3.844 0.000

2 0.944 0.037 25.746 0.000

3 0.616 0.180 3.430 0.001

4 0.434 0.056 7.694 0.000

5 -0.190 0.257 -0.740 0.463

6 -5.526 1.437 -3.844 0.000

7 0.944 0.037 25.746 0.000

8 0.616 0.180 3.430 0.001

9 0.434 0.056 7.694 0.000

10 -0.190 0.257 -0.740 0.463

*********************************************************

Value p-value

F 2.487 0.044

Wald 15.028 0.010

LR 13.363 0.020

Score 11.936 0.036

Display Code ends for publication

disp('code ends')

code ends

Functions

function [b, varb, e] = mc_olsr(y, x, R, r, names, silent, regularvc) %{ Copyright (C) 2010 Michael Creel <michael.creel@uab.es> This program is free software; you can redistribute it and/or modify it under the terms of the GNU General Public License as published by the Free Software Foundation Calculates restricted LS estimator (subject to Rb=r) using the Huber-White heteroscedastic consistent variance estimator. inputs: y: dep variable x: matrix of regressors R: matrix R in Rb=r r: vector r in Rb=r names (optional) names of regressors silent (bool) default false. controls screen output regularvc (bool) default false. use normal varcov estimator, instead of het consistent (default) outputs: b: estimated coefficients varb: estimated covariance matrix of coefficients (Huber-White by default, ordinary OLS if requested with switch) e: ols residuals ess: sum of squared residuals %} if nargin < 7 regularvc = false; end if nargin < 6 silent = false; end k = size(x,2); if (nargin < 5) || (size(names,1) ~= k) names = 1:k; names = names'; end [b, sigsq, e] = ols(y, x); xx_inv = inv(x'*x); n = size(x,1); k = size(x,2); q = size(R,1); try P_inv = inv(R*xx_inv*R'); catch der_stop = 1; end b = b - xx_inv*R'*P_inv*(R*b-r); e = y-x*b; ess = e' * e; sigsq = ess/(n - k - q); % Ordinary or het. consistent variance estimate if regularvc==1 varb = xx_inv*sigsq; else varb = HetConsistentVariance(x,e); end A = eye(k) - xx_inv*R'*P_inv*R; %# the matrix relating b and b_r varb = A*varb*A'; seb = sqrt(diag(varb)); t = b./seb; tss = y - mean(y); tss = tss' * tss; rsq = 1 - ess / tss; labels = char('estimate', 'st.err.', 't-stat.', 'p-value'); if silent==0 ('\n*********************************************************\n'); fprintf('Restricted LS estimation results\n'); fprintf('Observations %d\n',n); fprintf('R-squared %f\n',rsq); fprintf('Sigma-squared %f\n',sigsq); p = 2 - 2*tcdf(abs(t), n - k - q); results = [b, seb, t, p]; if regularvc==1 fprintf('\nResults (Ordinary var-cov estimator)\n\n'); else fprintf('\nResults (Het. consistent var-cov estimator)\n\n'); end prettyprint(results, names, labels); fprintf('\n*********************************************************\n'); end end % function varb = HetConsistentVariance(x, e) xx_inv = inv(x'*x); E = e .^2; varb = xx_inv * x'*eemult_mv(x, E) * xx_inv; end %} function [F, W, LR, S] = TestStatistics(y, x, R, r) %{ Copyright (C) 2010 Michael Creel <michael.creel@uab.es> This program is free software; you can redistribute it and/or modify it under the terms of the GNU General Public License as published by the Free Software Foundation This code calculates F, Wald, Score and Likelihood Ratio tests for linear model y=XB+e e~N(0,sig^2*I_n) subject to linear restrictions RB=r The null is H_{0}:RB=r inputs: y: nx1 dependent variable x: nxk regressor matrix R: R above, a qxk matrix r: r above, a qx1 vector output: F: the F statistic W: the Wald statistic S: the score statistic LR: the likelihood ratio statistic %} n = size(x,1); k = size(x,2); q = size(R,1); % OLS [b, ~, ~] = ols(y, x); % The restricted estimator xx_inv = inv(x'*x); P_inv = inv(R*xx_inv*R'); b_r = b - xx_inv*R'*P_inv*(R*b-r); % Sums of squared errors and estimators of sig^2 e = y - x*b; ess = e'*e; e_r = y - x*b_r; ess_r = e_r' * e_r; sigsqhat_ols = ess/(n-k); sigsqhat_mle = ess/(n); sigsqhat_mle_r = ess_r/(n); % F-test F = (ess_r-ess)/q; F = F/sigsqhat_ols; % Wald test (uses unrestricted model's est. of sig^2 W = (R*b-r)'*P_inv*(R*b-r)/sigsqhat_mle; % Score test (uses restricted model's est. of sig^2 P_x = x * xx_inv * x'; S = e_r' * P_x * e_r/(sigsqhat_mle_r); % LR test lnl = -n/2*log(2*pi) - n/2*log(sigsqhat_mle) - e' * e/(2*sigsqhat_mle); lnl_r = -n/2*log(2*pi) - n/2*log(sigsqhat_mle_r) - e_r' * e_r/(2*sigsqhat_mle_r); LR = 2*(lnl-lnl_r); tests = [F;W;LR;S]; WLRS = [W;LR;S]; pvalues = [1 - fcdf(F,q,n-k); 1 - chi2cdf(WLRS,q)]; tests = [tests, pvalues]; TESTS = str2mat("F","Wald","LR","Score"); labels = str2mat("Value","p-value "); prettyprint(tests, TESTS, labels); end function [beta,sigma,r]= ols(y,x) % Simple OLS regression t = size(x,1); beta = inv (x'*x) * x' * y; sigma = (y-x*beta)'*(y-x*beta)/(t-rank(x)); r = y - x*beta; end function prettyprint(mat, rlabels, clabels) %{ This function prints matrices with row and column labels Copyright (C) 2010 Michael Creel <michael.creel@uab.es> This program is free software; you can redistribute it and/or modify it under the terms of the GNU General Public License as published by the Free Software Foundation %} % left pad the column labels a = size(rlabels,2); for i = 1:a fprintf(' '); end fprintf(' '); % print the column labels try clabels = [' ';clabels]; % pad to 8 characters wide catch dert_stop = 1; end clabels = strjust(clabels,'right'); k = size(mat,2); for i = 1:k fprintf('%s ',clabels(i+1,:)); end % now print the row labels and rows fprintf('\n'); k = size(mat,1); for i = 1:k if ischar(rlabels(i,:)) fprintf(rlabels(i,:)); else fprintf('%i', rlabels(i,:)); end fprintf(' %10.3f', mat(i,:)); fprintf('\n'); end end function result = eemult_mv(m,v) if not(ismatrix(m)) error("eemult_mv: first arg must be a matrix"); end if not(isvector(v)) error("eemult_mv: second arg must be a vector"); end [rm, cm] = size(m); [rv, cv] = size(v); if (rm == rv) v = kron(v, ones(1,cm)); result = m .* v; elseif (cm == cv) v = kron(v, ones(rm, 1)); result = m .* v; else error("eemult_mv: dimension of vector must match one of the dimensions of the matrix"); end end function [b, varb, e, ess] = mc_ols(y, x, names, silent, regularvc) %{ Copyright (C) 2010 Michael Creel <michael.creel@uab.es> This program is free software; you can redistribute it and/or modify it under the terms of the GNU General Public License as published by the Free Software Foundation Calculates ordinary LS estimator using the Huber-White heteroscedastic consistent variance estimator. inputs: y: dep variable x: matrix of regressors names (optional) names of regressors silent (bool) default false. controls screen output regularvc (bool) default false. use normal varcov estimator, instead of het consistent (default) outputs: b: estimated coefficients varb: estimated covariance matrix of coefficients (Huber-White by default, ordinary OLS if requested with switch) e: ols residuals ess: sum of squared residuals %} k = size(x,2); if nargin < 5 regularvc = 0; end if nargin < 4 silent = 0; end if (nargin < 3) || (size(names,1) ~= k) names = 1:k; names = names'; end [b, sigsq, e] = ols(y,x); xx_inv = inv(x'*x); n = size(x,1); ess = e' * e; % Ordinary or het. consistent variance estimate if regularvc==1 varb = xx_inv*sigsq; else varb = HetConsistentVariance(x,e); end seb = sqrt(diag(varb)); t = b ./ seb; tss = y - mean(y); tss = tss' * tss; rsq = 1 - ess / tss; labels = char('estimate', 'st.err.', 't-stat.', 'p-value'); if silent==0 fprintf('\n*********************************************************\n'); fprintf('OLS estimation results\n'); fprintf('Observations %d\n',n); fprintf('R-squared %f\n',rsq); fprintf('Sigma-squared %f\n',sigsq); p = 2 - 2*tcdf(abs(t), n - k); results = [b, seb, t, p]; if regularvc fprintf('\nResults (Ordinary var-cov estimator)\n\n'); else fprintf('\nResults (Het. consistent var-cov estimator)\n\n'); end prettyprint(results, names, labels); fprintf('\n*********************************************************\n'); end end

Restricted LS estimation results

Observations 145

R-squared 0.925652

Sigma-squared 0.155686

Results (Het. consistent var-cov estimator)

estimate st.err. t-stat. p-value

1 -4.691 0.804 -5.838 0.000

2 0.721 0.032 22.516 0.000

3 0.593 0.167 3.556 0.001

4 0.414 0.072 5.768 0.000

5 -0.007 0.154 -0.048 0.962

*********************************************************

Value p-value

F 0.574 0.450

Wald 0.594 0.441

LR 0.593 0.441

Score 0.592 0.442